Manish Choudhary

CEO & Co-founder, Ferry | Flexprice

Revenue on your income statement and cash in your bank account are not the same number, and the space between them is your receivables. Accounts receivable turnover is the metric that tells you how fast that space closes. Book a million in sales and collect it in 30 days, and you have a healthy business. Book the same million and collect it in 90, and you have a financing problem dressed up as growth.

TL;DR

Accounts receivable turnover measures how many times you collect your average receivables during a period, usually a year.

The formula is net credit sales divided by average accounts receivable. Convert it to days with 365 ÷ ratio, and that's your DSO.

There is no universal "good" number. Ratios around 7 to 10 are often healthy, but it depends on your industry and how you bill.

The ratio tells you collections are slow. It does not tell you which customers are dragging it down. That is its real limit.

What is accounts receivable turnover?

Accounts receivable turnover is a ratio that measures how many times a company collects its average accounts receivable over a set period. Accounts receivable is the money customers owe you for sales you have already made on credit. The ratio, also called the receivables turnover ratio or AR turnover ratio, is a read on one thing: how efficiently you turn those credit sales back into cash.

A higher number means you collect quickly. A lower number means cash is sitting in receivables longer than you would like. On its own it is just a number, so the rest of this guide is about how to calculate it and, more importantly, how to read it.

What is the accounts receivable turnover formula?

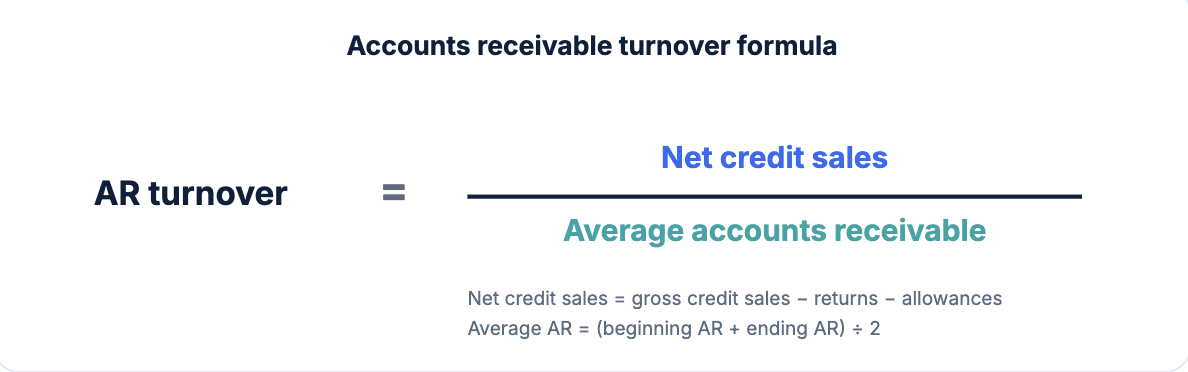

The accounts receivable turnover formula is net credit sales divided by average accounts receivable.

Accounts receivable turnover = Net credit sales ÷ Average accounts receivable

Both inputs matter, and getting either one wrong quietly breaks the result. Here is what each one means.

What counts as net credit sales?

Net credit sales are your sales made on credit, minus returns and allowances. The "credit" part is the piece people miss. You exclude cash sales entirely, because a cash sale never creates a receivable, so including it inflates the ratio and tells you nothing useful. Net credit sales = gross credit sales − returns − allowances.

How do you calculate average accounts receivable?

Average accounts receivable is the beginning AR balance plus the ending AR balance, divided by two. You average the two because a single point-in-time balance swings with billing timing, especially if you invoice heavily at month-end. Average AR = (beginning AR + ending AR) ÷ 2.

Accounts receivable turnover example

Here is the full calculation with real numbers. Say a company had $1,200,000 in net credit sales last year. Its receivables were $130,000 at the start of the year and $170,000 at the end.

First, average AR = ($130,000 + $170,000) ÷ 2 = $150,000. Then, AR turnover = $1,200,000 ÷ $150,000 = 8.

So this company collected its average receivables eight times over the year. By itself, eight does not mean much. It starts to mean something the moment you turn it into days and compare it against your payment terms, which is the next step.

How do you convert turnover to days?

To convert the ratio into days, divide 365 by your turnover ratio. This gives you the average collection period, the typical number of days it takes to collect an invoice. It is the same metric as days sales outstanding (DSO), just expressed in time instead of frequency.

Using the example above: 365 ÷ 8 = about 46 days. Now the number talks. If that company sells on net-30 terms, a 46-day collection period means customers are paying roughly two weeks late on average, which is a collections problem worth investigating. If it sells on net-45 terms, 46 days is basically on schedule. The average collection period formula is simply 365 ÷ AR turnover ratio, and it is the version of this metric most people find easier to act on.

What is a good accounts receivable turnover ratio?

There is no single good accounts receivable turnover ratio, because what counts as healthy depends entirely on your industry and how you bill. As a loose benchmark, ratios in the 7 to 10 range are often considered healthy, and some sources put the cross-industry average near 7.8. But a grocery store and a construction firm live in completely different worlds, so the only comparison that means anything is against your own industry and your own past trend.

It also helps to know that both extremes cut both ways. A high ratio usually signals fast, efficient collections, but it can also mean your credit terms are so strict that you are turning away good customers. A low ratio often points to slow collections or lenient terms, but it can be perfectly normal for businesses that bill on milestones, retainers, or long project cycles. Read the number in context, never in isolation.

Why the ratio can lie to you

The accounts receivable turnover ratio is a company-wide average, and averages hide things. A perfectly healthy-looking ratio of 9 can sit on top of three enormous accounts that pay 60 days late, with a long tail of small customers paying on time pulling the average back up. The metric tells you the building is roughly fine. It does not point at the room that's on fire.

Your billing model distorts it too. A company that bills annually upfront will post a high turnover ratio almost automatically, while a usage-based or arrears-billed company carries structurally higher average receivables and posts a lower ratio, even when its collections team is doing everything right. For the SaaS and usage-based businesses I work with, this trips people up constantly: the headline ratio looks worse than the collections actually are, purely because of when invoices go out. So treat turnover as the opening question, not the verdict.

Common mistakes that break the calculation

A few small errors turn this metric into noise. The three I see most often: using total sales instead of net credit sales, which counts cash revenue that never created a receivable; using the ending AR balance instead of the average, which lets billing timing swing the result; and mixing time periods, like dividing annual sales by a single quarter's average AR. Each one produces a number that looks fine and means nothing.

How Ferry's AI agent tracks turnover customer by customer

Ferry's AI agent tracks AR aging and DSO at the account level, so you can see which specific customers are dragging your turnover down instead of just watching a company-wide average drift. Ferry's agent ranks customers by collection risk, flags accounts heading toward bad debt before they get there, and ties every figure on the dashboard back to the source contract and the usage behind it, so a falling ratio comes with names attached rather than a mystery to investigate.

From there, Ferry's agent runs dunning tailored to each cohort to lift collections where they are actually slow, and applies incoming cash automatically so the numbers stay current. One founding engineer at Segwise, Kush Daga, described the shift this way: "Our revenue reporting is now backed by complete AR visibility. Every number drills down to the invoice and the usage behind it, no more reconciliation spreadsheets." Customers using the real-time revenue reporting have reported cutting DSO by more than 60%. If the ratio is telling you collections are slow, this is how you find out where. For the follow-up side of that, see our guide to dunning letters.

The ratio is a question, not an answer

Accounts receivable turnover is one of the fastest ways to check whether your sales are actually turning into cash, but it is a starting point, not a diagnosis. Calculate it, convert it to days, and compare it to your terms. Then do the part that actually moves cash: drill into the accounts behind the number and find the ones that are late. The ratio will tell you something is slow. Your customer-level data is what tells you where to go fix it.

What is a good accounts receivable turnover ratio?

How do you calculate accounts receivable turnover?

What is the difference between AR turnover and DSO?

Is a high accounts receivable turnover ratio good?

What is the average collection period formula?